Log in to learn from real founders, exchange ideas, and work on businesses that move from concept to execution.

Access Knowasiak

Join the conversations shaping real businesses.

Global Hybrid Truck Market Analysis: Growth Drivers, Trends, and Forecast (2025–2032)

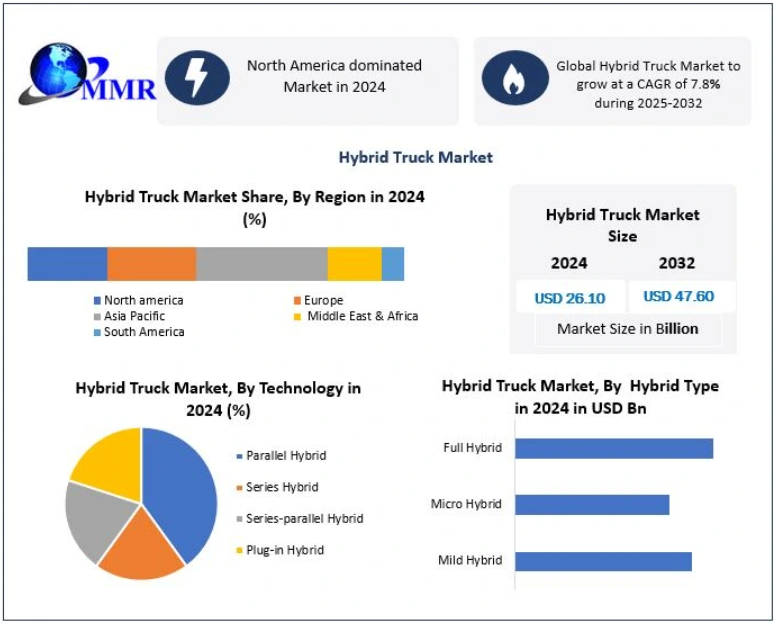

The Global Hybrid Truck Market was valued at USD 26.10 billion in 2024 and is projected to expand at a CAGR of 7.8% between 2025 and 2032, reaching an estimated USD 47.60 billion by 2032. Market growth is being fueled by tightening emission regulations, rising urban freight activity, and the need for transitional powertrain solutions ahead of full electrification.

Market Overview

Hybrid trucks are commercial vehicles that combine internal combustion engines (ICE) with electric propulsion systems to improve fuel efficiency, reduce emissions, and lower operating costs. These vehicles are deployed across light-, medium-, and heavy-duty segments, utilizing technologies such as parallel hybrids, series hybrids, and plug-in hybrids.

The market is positioned as a critical bridge between conventional diesel trucks and fully electric or hydrogen-powered alternatives. Increasing pressure on OEMs to meet emission norms, combined with fleet operators’ demand for cost-effective decarbonization, is accelerating hybrid truck adoption globally. Public transit agencies, municipal fleets, and last-mile delivery operators are among the earliest adopters, given predictable routes and urban operating environments.

To know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/77705/

Market Dynamics

Stringent Emission Regulations Accelerating Market Growth

Rising global concerns over air quality and climate change have prompted governments to enforce stricter emission standards for commercial vehicles. Regulatory frameworks such as Corporate Average Fuel Economy (CAFE) standards in the U.S. and carbon reduction mandates across Europe are compelling manufacturers to adopt hybrid and electric powertrains.

Hybrid trucks emit significantly fewer greenhouse gases compared to conventional diesel vehicles, making them an attractive compliance solution. In medium- and heavy-duty vehicles (MHDVs), electrification offers substantial fuel savings, particularly in stop-and-go urban conditions where regenerative braking enhances energy recovery. Advances in battery performance and declining costs over the last decade have further improved the commercial viability of hybrid powertrains.

Public transport remains a major catalyst. Electric and hybrid buses dominate the electrified commercial vehicle landscape, especially in China, Europe, and parts of North America. Strong policy support, subsidies, and pilot programs have enabled transit agencies to scale hybrid adoption, creating spillover demand across adjacent truck segments.

Growing Competition from Battery Electric and Fuel Cell Vehicles

Despite strong momentum, the hybrid truck market faces competition from battery electric vehicles (BEVs) and fuel cell electric vehicles (FCEVs). Rapid improvements in BEV range, charging infrastructure, and total cost of ownership are encouraging fleet operators to bypass hybrid solutions altogether.

Fuel cell vehicles, offering long range, fast refueling, and zero tailpipe emissions, are gaining attention—particularly for long-haul and heavy-duty applications. Governments are actively supporting hydrogen mobility through funding and infrastructure development, which could limit long-term hybrid adoption. However, high costs and limited hydrogen availability continue to restrict near-term scalability, keeping hybrids relevant as a transitional technology.

Market Segmentation Analysis

By Powertrain Type

The hybrid truck market is segmented into parallel hybrids and series hybrids.

Parallel hybrid systems are expected to account for the largest market share throughout the forecast period. Their dominance is driven by lower system costs, simpler architecture, and widespread use of regenerative braking. These systems recover kinetic energy during braking and convert it into electrical energy, reducing dependence on external charging infrastructure and improving fuel economy in urban driving conditions.

By Vehicle Type

Based on vehicle type, the market is categorized into light-duty, medium-duty, and heavy-duty trucks.

Light-duty trucks, including hybrid pickup trucks and delivery vans, currently lead the market due to ease of electrification, strong demand from e-commerce and urban logistics, and supportive emission policies.

Medium-duty trucks are widely used in municipal services, waste management, and short-range distribution, benefiting from balanced payload capacity and operating efficiency.

Heavy-duty trucks show slower adoption due to higher power demands and system complexity, though hybridization is increasingly explored for vocational and regional haul applications.

To know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/77705/

Regional Analysis

North America Leads Global Market

North America dominated the hybrid truck market in 2024, supported by strict emission regulations, generous incentives, and a well-developed commercial vehicle ecosystem. The U.S. and Canada have actively promoted cleaner freight solutions, encouraging fleet electrification through grants and tax credits.

The region benefits from the strong presence of major OEMs such as Ford, General Motors, and PACCAR, along with high fleet renewal rates. While Asia Pacific is the fastest-growing region—driven by large-scale production in China, Japan, and India—North America remains the most commercially mature market. Europe also plays a significant role but trails North America and APAC in overall scale.

Competitive Landscape

The hybrid truck market is shaped by intense competition among global OEMs, with Volvo Group, BYD Auto, and Ford Motor Company emerging as key influencers.

Volvo Group leads in medium- and heavy-duty hybrid solutions, leveraging advanced powertrain engineering, strong European demand, and integrated fleet services.

BYD Auto benefits from China’s supportive EV policies and vertically integrated battery manufacturing, enabling cost control and rapid global expansion across Asia, Latin America, and emerging markets.

Ford Motor Company dominates the light-duty hybrid segment in North America, particularly with hybrid pickup models. While its innovation in connectivity and onboard power systems is notable, scaling hybrid technology into heavier truck classes remains a strategic challenge.

Future leadership will depend on battery ecosystem control, regulatory alignment, and adaptability across diverse fleet use cases.

Market Trends

Advanced Hybrid Architectures: OEMs are developing diverse hybrid configurations, including plug-in hybrids and range-extended systems, to improve towing capacity, efficiency, and operational flexibility.

Technology Integration: Features such as regenerative braking, AI-based energy management, telematics, and vehicle-to-load power systems are enhancing fleet value propositions.

Policy-Driven Adoption: Emission mandates and incentives are accelerating the rollout of plug-in and heavy-duty hybrid trucks as transitional solutions before full electrification.

Recent Developments

Recent industry developments highlight strategic shifts toward hybridization:

Launch of new plug-in hybrid pickups in China and global markets

OEM mergers and alliances aimed at accelerating clean-energy truck development

Strategic acquisitions strengthening hybrid drivetrain and component manufacturing capabilities

Global expansion of hybrid truck platforms into Latin America and Asia Pacific

Conclusion

The global hybrid truck market is positioned for sustained growth as governments, fleet operators, and manufacturers seek practical decarbonization pathways. While full electrification remains the long-term objective, hybrid trucks offer a cost-effective and scalable solution in the near to medium term. Advances in powertrain technology, supportive regulations, and expanding urban logistics will continue to reinforce the market’s role in the evolving commercial vehicle landscape.